-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

Shock, Part 2 (The Asset Allocator's Dilemma)

Published: 11-28-2016

In Shock (Part 1) (http://blog.angelesadvisors.com/2016/11/shock-part-1/), we looked at a possible Trump economic agenda and its consequences. A large increase in government spending, tax cuts and deregulation will likely boost GDP growth in the near-term, while restrictions on trade and immigration are headwinds to growth. These policies will add to the inflationary pressures that have already been building.

Markets responded immediately to this agenda. US stocks rose to record levels, led by domestically-focused small cap companies, pharmaceuticals and banks, the prime beneficiaries of less future regulation. Trade-dependent emerging markets were sold, as were bonds, which offer little protection in an inflationary environment.

But some facts remain irrespective of who occupies the White House. Long-term, I remain bullish on US equities. But investors face two broad challenges: low returns and proper diversification.

Over the last 10 years ending October 31, a period that includes the financial collapse of 2008, US stocks averaged an annual return of 6.7%, and US bonds saw performance of 4.6% p.a. With CPI averaging just 1.7% in the decade, stocks gave us five full percentage points above inflation, and bonds added nearly 3% in real terms.

It is very unlikely investors will enjoy these levels of returns in the future. The past few decades saw a confluence of highly favorable developments. Inflation, and interest rates, fell from very high levels, to the lowest on record. Global growth was boosted by a rapid expansion of trade, gains in efficiency and productivity, and the entry of a few billion new producers and consumers into the world economy. All of these trends are either coming to an end or have already reversed. Future returns will be lower than what we’ve enjoyed in recent decades.

A fundamental principle of investing is diversification. What we really mean by diversification is a range of investments that have low, or negative, correlation with each other. That way, losses in one part of the portfolio are limited, while other areas of the portfolio are likely performing well. Since we don’t know which strategy or asset class will do well in the coming period, a well-diversified portfolio should enable investors to capture the best, while mitigating the worst, areas. The result is a more efficient portfolio, one with a better ratio of return and risk.

Stocks and bonds are the fundamental assets in portfolios, as these capture the broad macroeconomic forces of economic growth and contraction, inflation and deflation. Stocks and bonds thus represent opposing areas of the return/risk spectrum, acting as a natural hedge to the other.

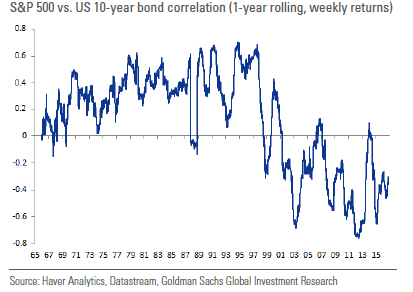

For the past two decades, this played out well: the correlation between equities and Treasuries was consistently negative. Investment alchemists (i.e., asset allocators, such as ourselves) were able to conjure up well-diversified, well-balanced, more efficient portfolios by taking advantage of this natural hedge between stocks and bonds.

But the negative equity/bond correlation we’ve enjoyed for the past 20 years is not necessarily the natural order of the investment universe and, in fact, was a reversal of the order of the previous three decades. The 1970s bear market in equities was coincident with a bear market in bonds. The 1980s and 1990s was a period of bull markets for both stocks and bonds. So, it appears, the equity/bond correlation is not really stable, much less “naturally” negative.

Correlation is not causation, as every statistics professor warns, but it makes sense that the economic environment is a critical determinant of the equity-bond relationship. A positive correlation exists when there is stronger nominal GDP growth, with higher levels of inflation and interest rates. A period of low growth and low inflation, which characterizes the past decade or two, is associated with a negative correlation between stocks and bonds.

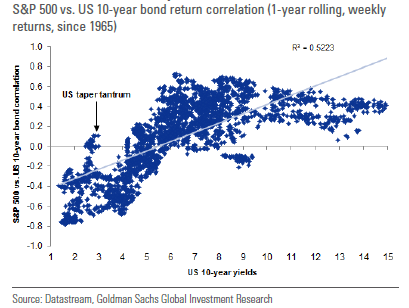

But at extremely low yields, the correlation turns more positive. It may be that at very low rates, bonds offer little yield protection from macroeconomic disruptions, and are thus a much less effective hedge for equities. This is exactly what we’ve seen recently, as the equity-bond correlation has been positive on days when equities have sold off.

If the equity/bond correlation is indeed reversing to a more positive one, as existed in the three decades before the late 1990s, our portfolios will become less efficient. That won’t matter much if the global economy can expand in real terms (1980s/1990s). But should growth slow and/or inflation rise (1970s), investors will be severely challenged.

The macroeconomic environment for the past few decades has been particularly advantageous to investors. The global labor force doubled, with the entry of China and other countries into the world economy. Trade soared at twice the pace of global growth, technology improved productivity and profits. Inflation and interest rates dropped from record highs to record lows. It has been a golden era for capital.

That era is not necessarily over. Policies that promote trade and basic research, reduce and simplify regulations and taxes and subsidies, can extend real global growth. Some of the recent campaign rhetoric was so aligned, but much of it wasn’t.

In next segment, I’ll examine some of the broader (non-economic) implications of this new era.

Print this Article-

![Balance]() 29 Oct, 2019

29 Oct, 2019Balance

October 1987 was a memorable month for me. It began with the 5.9 magnitude Whittier Narrows quake that rocked my ...

-

![Beach Reading]() 13 Aug, 2024

13 Aug, 2024Beach Reading

Six new books for you, all fiction, all great. I hope you enjoy!The Sellout, Paul BeattyThis is possibly the most ...

-

![Im Not Dead!]() 24 Oct, 2014

24 Oct, 2014Im Not Dead!

A great line from a great Monty Python movie, and another crisp cover from The Economist: ...

-