-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

The Present is the Future (at least in bond land)

Published: 10-27-2014In our long-term assumptions, we generally assume that the total return in fixed income is pretty close to its starting yield. That’s because a bond’s total return is a function of two variables: yield and re-investment yield. As yields move up and down, bond prices move inversely, down and up, but the re-investment rate moves positively with yields. In the short-term, changes in prices have a large impact on total return, but given enough time, the re-investment yield (almost) completely offsets the price/yield function.

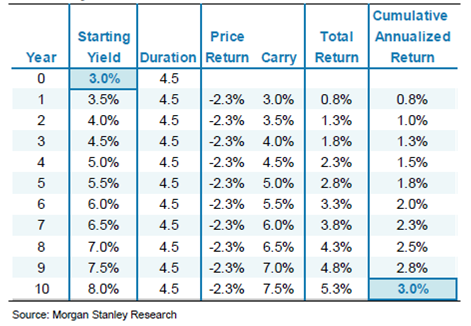

The table below (courtesy Morgan Stanley), shows the effect of interest rates rising from 3% to 8% at 50 basis points a year over 10 years. The total return over this decade works out mathematically to 3%, (not) coincidentally the starting yield.

There are risks to owning bonds, primarily higher inflation, and to a lesser extent default risk. But the laws of mathematics make us highly confident that the long-term nominal return for bond investors will be right around today’s yield.

Print this Article

-

![Party Like It's 1999?]() 12 Jun, 2015

12 Jun, 2015Party Like It's 1999?

Some observers point to the eye-popping valuations for companies with little revenue (WhatsApp, e.g., bought by Facebook ...

-

![Fairy Tales]() 19 Nov, 2015

19 Nov, 2015Fairy Tales

The technology bubble of the late 1990s is a distant memory for most investors, and an ignorance for the rest. But back ...

-

![MLPs]() 15 Oct, 2014

15 Oct, 2014MLPs

Some historical data from Credit Suisse below: MLPs are off 14% this month, pretty bad. Subsequent performance (no ...

-